What Is a Good Cap Rate for Rental Property?

To be a successful real estate investor, you need to use numerous metrics before buying a property. From cap rate to estimated cash flow, certain...

6 min read

When you add a piece of real estate to your investment portfolio, you'll earn passive income from any increases to the property value as well as any rents you collect. Soon after the COVID-19 pandemic began, the Federal Reserve dropped the fed funds rate to keep the economy afloat, which resulted in substantial interest rate reductions on mortgages and other loan types.

Over the past year, the Fed has increased interest rates to combat inflation. Since then, many investors and potential homeowners have shied away from making a purchase. However, history shows us that we've been pampered in recent years. The following offers a closer look at owner-occupied properties and the interest rates they come with. It should be noted that owner occupancy rates are lower, and investor rates are going to be about 1.5 to 2.0 percent higher due to the perceived risk of loaning to investors who don’t live in the house.

Owner-occupied properties are pieces of real estate where the individual who purchases the property and holds the title will use it as their main residence. The owner-occupied term is most often used to describe investors who choose to live on the property that they've purchased. At the same time, they will rent out any additional units to tenants.

When it comes to real estate investing, owner-occupied properties give you the ability to take advantage of appealing financing solutions. Purchasing a property that you live in allows you to tap into much better loan terms and interest rates when compared to more traditional real estate investments. Even though interest rates are relatively high at the moment, making an owner-occupied investment can still be highly rewarding.

While investors can benefit from great financing options that are usually restricted to homeowners, there are certain requirements that must be met before the loan approval will be given. First of all, you'll be tasked with moving into the home within a period of 60 days following closing. You must also live there for at least one year if you want to be considered an owner-occupant with your lender.

It may be possible to gain financing even if you're an absentee owner. In this scenario, the owner doesn't live on the property. For instance, when a property owner decides to rent out their single-family home, they would be viewed as an absentee owner. Every lender has its own set of occupancy rules and guidelines. You should look through the finer details of your lender's requirements for owner occupancy to avoid mortgage fraud.

Before you invest in owner-occupied real estate, you should understand the pros and cons of this investment strategy. The main benefit of investing in an owner-occupied property is that you'll have just one mortgage for your investment property and primary home, which makes it easier to remain current on your payments.

If you use this strategy to purchase a multifamily property, you'll live near all of your tenants, which allows you to react quickly in case of an emergency. Living on-site also allows for more streamlined maintenance of your property. Keep in mind that some loans can only be obtained by owner occupants.

One notable downside to purchasing owner-occupied properties is that you could live alongside noisy neighbors. With a multifamily property, you'll be in close proximity to your tenants. It may also be more challenging to find tenants who are willing to live in the same place as their landlord. If you can't find enough tenants, vacancies are a distinct possibility.

As a landlord, you don't earn passive income. You're tasked with maintaining the property and taking care of all tenant issues. If you want to avoid these tasks, you can hire a property management company to handle the day-to-day operation of the property.

As interest rates have climbed over the past 12 months, many investors have become wary of adding properties to their portfolio because of the high cost of owning a home. There are, however, different factors that impact your interest rate. These factors include:

If your credit score is higher than 800 and your financials are strong, you'll likely qualify for an interest rate that's lower than the average. You also have the ability to negotiate mortgage rates. Interest rates can be lowered with discount points, which require you to pay cash up front.

A credit score that's higher than 720 makes it more likely that you'll receive a low-interest-rate mortgage. Loan programs like VA, USDA, and FHA loans are available to borrowers with a credit score below 600. Before you borrow money to purchase an owner-occupied home, give yourself some time to raise your credit score. Doing so can save you thousands of dollars.

A down payment allows you to lower your borrowing rate if it's high enough. The majority of mortgages require a down payment that amounts to at least 3-3.5% of the home value. USDA and VA loans can be obtained with no down payment. However, providing a down payment of anywhere from 10-20% might allow you to obtain a conventional loan with low interest rates and no private mortgage insurance.

Ready to invest? Check out our guide on investment property down payments!

The type of loan you apply for can also impact your interest rate. Keep in mind that the loans you qualify for depend on your current credit score. If your credit score is less than 600, government-backed loans might be the only ones available to you. While FHA loans have relatively low interest rates, they always require borrowers to have mortgage insurance.

You can receive lower interest rates with an adjustable-rate mortgage. However, the rate will change following the initial period where the rate is fixed, which can be anywhere from 5-10 years.

If you opt for a 15-year mortgage as opposed to a 30-year one, you'll receive a lower interest rate. While your monthly payment would be higher as a result of the short loan term, your total costs would drop significantly because of the much lower interest charges.

As for the loan amount, a smaller home loan doesn't always equate to a lower interest rate. If the home loan is $50,000 or less, your interest rate will likely be higher to offset the lower profits that the lender will be bringing in. Jumbo mortgages also come with higher interest rates. For multifamily properties, jumbo mortgages can be as high as $3.5 million.

The discount points mentioned previously allow you to reduce your interest rates by around 0.25% when you pay a certain amount of cash. A single discount point requires you to pay 1% of your home loan amount. If the loan is $300,000, you would pay $3,000 for a discount point. You would eventually recover the upfront expenses by obtaining a lower interest rate.

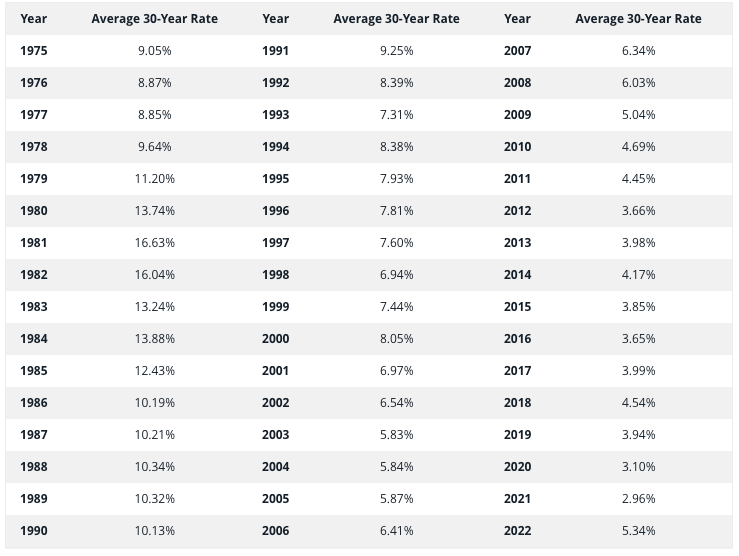

The average interest rate by year is:

Today's average interest rate is 6.76%.

It's a common belief among investors and prospective homeowners alike that interest rates are too high and need to drop immediately to make owning a home more affordable. In reality, interest rates only seem high because they've been kept low for a lengthy period of time. Even before the Federal Reserve dropped the fed funds rate after the COVID-19 pandemic, the average interest rate hadn't been above 5% since 2009. After 2000, interest rates never went higher than 7% until a brief period in 2023.

While a 6% interest rate isn't necessarily low, you should consider the history of interest rates on owner-occupied properties. In the 1980s, people looking to purchase a home would often pay interest rates between 10-30%. In fact, the average interest rate in 1981 was 16.63%. The highest interest rate that year was 18.6%, which took place in October. Interest rates would stay in double digits until 1991, which is when the average rate settled in at 9.25%. In the decade that followed, the lowest interest rate for a 30-year, fixed-rate mortgage was 6.94%.

One of the reasons why interest rates were once so high is because homes were much less expensive. In 1983, the average price for a single-family home was just $75,300. If the interest rate was 16% on a 30-year mortgage, the monthly mortgage payment would be just over $1,000, which was around 50% of the median income in 1983. In comparison, the modern investor or homeowner has it much better.

Interest rates were also high during the 1980s because of credit not being as widely available, which meant that it was more expensive for buyers to obtain a mortgage. With less credit to provide, banks were taking on more risk with each loan. Modern mortgages are usually bundled and placed into investment products that go on the secondary market. This market allows lenders to earn profits from providing loans to large quantities of borrowers, which is why it's unlikely that interest rates will get too high anytime soon.

When you look at today's average interest rate and see that it's around 6.76%, you may be frustrated at the idea that interest rates were below 3% early last year. However, historical data shows us that current rates are still relatively low. They are also significantly lower than what you would experience if you were investing in a property without intending to live in it. Investment properties typically come with interest rates that are 0.5-1.5% higher than owner-occupied properties.

Investing in an owner-occupied property allows you to benefit from high savings that can be added to your cash reserves, retirement account, or another investment property. Though interest rates are currently higher than they've been in years, they are also much lower than they were throughout the last two decades of the 20th century. An owner-occupied investment is still an effective technique for building your wealth.

To be a successful real estate investor, you need to use numerous metrics before buying a property. From cap rate to estimated cash flow, certain...

The anticipation of mortgage rate predictions holds significant implications for both individuals and the broader real estate market. Understanding...

There are so many terms that get thrown around when evaluating rental properties. For some they are second nature, but for others they are the...