401(k) vs. Real Estate: Which is Better for Retirement?

Today, many employees have a 401(k) plan as a means of saving for retirement. It was first introduced in 1978 and has since become the most commonly...

6 min read

Having a 401(k) plan with your employer will certainly help you save money for retirement. You can make a set amount of salary-reduction contributions to this account that will grow over time because of the interest rate that's tied to the account. If, however, your 401(k) is your sole source of income after retirement, it likely won't be enough to retire rich or early. Here's why a 401(k) account won't provide you with enough monthly income to live off of.

The type of 401(k) account you have determines what the exact rules and guidelines are. Two options at your disposal include a traditional 401(k) and a Roth 401(k). A traditional 401(k) will deduct all of your contributions from your gross income, which is your income before taxes have been deducted.

Your taxable income will be reduced by the amount of contributions you make to your 401(k) account throughout the year. These contributions can be reported as tax deductions on your annual return. You won't need to pay taxes on these funds until you end up withdrawing your money, which usually occurs after you reach retirement.

When it comes to a Roth 401(k), your contributions will be deducted from after-tax income. If you take this approach, you won't be able to claim a tax deduction for the year of the contribution. However, no additional taxes will need to be paid once you withdraw these funds in retirement. Keep in mind that not every employer provides employees with this type of retirement account.

The 401(k) has a lengthy history that began with the passing of the Revenue Act of 1978. Section 401(k) of this bill provided employees with a tax-free method of deferring some of the compensation they received from stock options or bonuses. The law officially went into effect at the beginning of 1980.

One year later, the Internal Revenue Service (IRS) issued guidelines that provided employees with the ability to place money into 401(k) plans via salary deductions, which is the main reason that these plans became widespread throughout the 1980s.

Companies preferred this solution since it was more affordable and predictable when compared to pensions. As for employees, they liked putting money into their 401(k) accounts because of the belief that these accounts would better position them for retirement.

Before the start of the 21st century, there were two bull-market runs that caused 401(k) accounts to be pushed higher in value. However, the market crash in 2008 resulted in many of these gains being erased and confidence in 401(k) accounts dropping among employees.

While some people have had second thoughts about 401(k) plans and their viability for building retirement savings, these accounts are still growing consistently. Despite their many advantages, they shouldn't be your main source of retirement income if you want to retire early or rich.

To understand why a 401(k) isn't enough to retire early, there are some statistics that you should be aware of. According to an analysis performed by Vanguard in 2021, the average balance on a 401(k) is around $129,157. If you plan to maintain these savings over a five-year period, your monthly income during retirement would be around $2,100.

The amount of money that an individual places into a 401(k) account largely depends on when they started saving and how often they made contributions. If you made sure to match the contribution limits each year, you may eventually have enough money to retire as a relatively wealthy individual. However, most people don't start making contributions early enough and will end up missing months or years of potential contributions because of a job loss.

Based on the statistics mentioned above, it's possible to calculate the amount of money you would need to put into your retirement account if you want to match your current annual income, which would allow you to maintain your standard of living.

To understand just how much money you would need to save in a 401(k) to have a comfortable life in retirement, let's say that you earn an expected return of around 6% for your 401(k) assets once you reach retirement. If you earn $150,000 at your current job and would like to be able to replace your entire income once you reach retirement, you would likely need upwards of $4 million in your 401(k) account.

In the event that you put money into your 401(k) for 30 years before you retire, you would end up with just under $2 million at the time of retirement. While this might be enough money to live off of for quite some time, it won't give you the same amount of income that you have access to while you're still working.

The way that you invest with your 401(k) also dictates how much money you'll have. It's common for individuals to switch to low-yield bonds and similar investments that are relatively safe. However, doing so would invariably lower your returns.

Before you invest in the stock market with your 401(k), keep in mind that the returns from these investments are unpredictable. If a market crash occurs right before you reach retirement age or in the first few years of retirement, your savings could take a big hit.

You should also know that inflation will factor into your overall savings. The average salary of $150,000 per year that you currently bring in will need to be much higher 30 years into the future to have the same purchasing power. Below are four of the issues and limitations associated with 401(k) accounts.

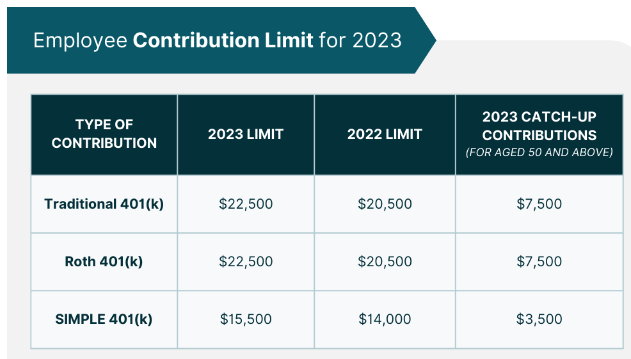

The main reason that you can't retire early or rich by investing in a 401(k) is because of the caps that are placed on contributions. IRS regulations dictate that employees can only contribute a small percentage of their salary into a 401(k). For 2022, the max contribution was $20,500. In 2023, the max contribution is increasing to $22,500. Individuals who are at least 50 years old can make a catch-up contribution of $6,500 in 2022 and $7,500 in 2023.

Employers are able to mitigate the issues associated with contribution caps by matching some of the contributions that you make. The limit for contribution matches has been set to $61,000 from all sources in 2022 and $66,000 from all sources in 2023. Annual additions can't be higher than 100% of your annual compensation. Even if you save the highest amount of money that's allowed each year, you likely won't have enough money for retirement.

Two issues that reduce your savings are taxes and inflation. Over time, the cost-of-living increases. Even if you're saving the amount of money that you believe will allow you to live comfortably, you can't be certain of how much inflation will increase before you reach retirement age. In this scenario, you may be tasked with downgrading your lifestyle.

Taxes can also be a problem. While 401(k) contributions are tax-deferred and grow without building any more taxes, the withdrawals you make during retirement will be taxed at the rate that matches your annual income. The $2 million you save in your 401(k) won't amount to $2 million in retirement because of the need to pay taxes. Plan on as much as 30% of your 401(k) to go away once taxes must be paid.

The impact of administrative fees on your 401(k) account can be high. It's possible for these costs to take up more than 50% of your savings. There are many undisclosed fees that can be found in a 401(k), which include legal fees, trustee fees, and bookkeeping fees.

It's also possible that you'll need to pay fund fees if you invest in mutual funds with your 401(k). In this scenario, these funds often obtain a 2% fee off the top. In the event that a mutual fund is set to pay out 7% annual returns but takes a 2% fee at the same time, you'll be left with a 5% return. This type of long-term compounding of fees must be taken into account.

Even though 401(k) accounts allow you to build funds for retirement, they don't have much liquidity. The money you place into a 401(k) is basically locked until you reach the right age or have an exception. Without this exception in place, you'll pay a sizable penalty if you take out an early withdrawal. When you withdraw funds before you reach 59.5 years old, you could face a 10% penalty that applies to the withdrawal amount.

All of your withdrawals will be taxable events. If you withdraw a high amount of money, you could push yourself up to a higher tax bracket, which increases your costs. The only exception to this rule is that you can borrow a small amount from your 401(k) as long as it's paid back within a set period of time.

Three alternative solutions that can help you build your wealth and add to the income you save with your 401(k) include:

Dividend-paying stocks allow you to build income in a slow but consistent manner. Well-known companies like McDonald's and Coca-Cola have been increasing their dividends for more than 20 years in a row, which means that people who invested decades ago have garnered exceedingly high yields on the initial investment.

Rental properties allow you to produce passive income as long as you pay for a property management company to handle maintenance, rent collection, and all other aspects of managing a property. Rents also tend to increase over time, which improves an investor's income.

Another option involves buying an S&P 500 index fund, which can generate high amounts of long-term wealth. The average long-term return for the S&P 500 is over 10%, which means that you could gain high rewards for a decent amount of risk.

Even though a 401(k) isn't sufficient for retirement, you can mitigate these issues by building your wealth through other methods. If all of your savings are tied up in a 401(k), you won't have much flexibility when it comes to withdrawals. The alternatives mentioned above are a good place to start.

Today, many employees have a 401(k) plan as a means of saving for retirement. It was first introduced in 1978 and has since become the most commonly...

We’ve all heard the fable: would you rather have $1,000,000 today or have a penny double every day for 30 days?

Investing in real estate for retirement is one of the savviest moves you can make for your financial future. Keep reading to learn about the benefits...